|

Originally published November 11, 2015 by Ash Ahluwalia at www.nsspartners.com.  Here we go again! Already one of the most complicated of government programs, the bipartisan Budget Bill signed last week has created a great deal of confusion and complication for those looking to social security to provide income in retirement.

Before the new legislation, there were over 2,700 rules governing social security. A typical couple had as many as 567 different flying options. Now, with the new legislation, their are even more rules and potential options depending on your age and marital status. In broad terms, there are now basically 4 different groups of social security beneficiaries with correspondingly different sets of filing rules to abide by:

For those in group #1, there will be no changes to their benefits, generally speaking, provided that they continue to receive their benefits as is and do not voluntarily suspend their benefits. For example, if the worker from whom spousal benefits are collected against were to voluntarily suspend receipt of their benefits (eg. in order to receive an 8% annual increase in benefits to age 70) after May 1,2016, then any spousal or children’s benefits paid against their record would also cease. For group #2, those individuals who will turn age 66 (or older) by May 1, 2016, there is still a very short “6 Month Window” of opportunity to take advantage of a filing strategy called “file and suspend”. For many clients eligible to do so, this filing strategy could provide as much as $50,000-$300,000 or more in additional lifetime social security benefits. After May 1, 2016, this filing option will no longer be available. CAUTION: It is critical to note that “file and suspend” may not always be the best filing option in all cases even for those still eligible to do so. In fact, in some cases it could actually result in a loss of as much as $50,000 or more in benefits. It’s critical for filers to consult with a social security income specialist before taking any action regarding “file and suspend”. Just because you may be eligible to do “file and suspend” doesn’t mean it will always be your best filing option. For those in group # 3, individuals who will turn age 62 or older by 12/31/15, there remains an abundance of valuable filing options available to enhance lifetime benefits. This is because the changes to the “deemed filing rules” do not apply to this group. As a result, there remain a number of filing strategies available to provide for spousal and divorced-spousal benefits which can significantly increase lifetime benefits. This can be a very complicated area of social security income maximization planning so it’s important to consult with a specialist in this area before filing. For group #4, virtually all of the “exotic” filing strategies will no longer be available. However, it’s important to understand just how valuable social security benefits still are. They typically provide for 30-60% of most filers income in retirement even without any special filing options. It’s best to think of social security benefits like a “big cake”. As a result of last week’s budget bill, most of the “icing” is off the cake for those who turn age 62 after 12/31/15. However, it remains a “very big cake”! For most retirees, social security remains their only true pension plan in retirement and can easily provide as much as $1 million or more in lifetime benefits for many couples in retirement. As a result of last week’s Budget Bill, it is more critical than ever to find out what your social security benefits will be under the new federal regulations, what would be the best time to file and what would be the best way to co-ordinate these benefits with your other retirement assets.

0 Comments

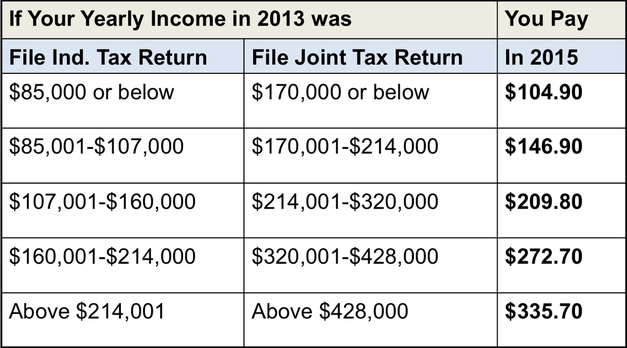

Centers for Medicaid & Medicare Services (CMS) sent out a bulletin yesterday with the official changes for 2016 with regards to Medicare Premiums, Deductibles and Co-Pays. The key changes are summarized below. Part B: Monthly Premiums increase ~15% The 2015 Part B Premiums are in the table above. The majority of people pay the $104.90/month in 2015.

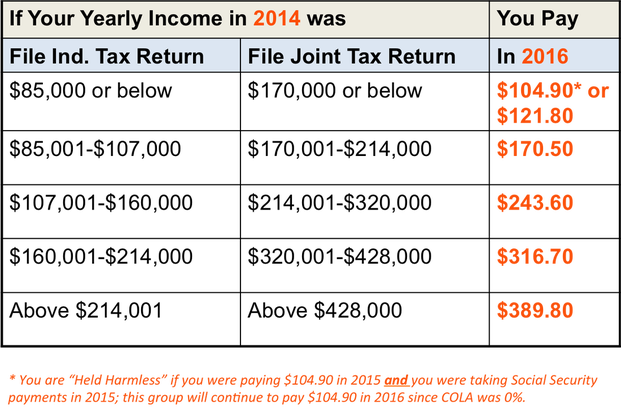

The 2016 Part B Premiums are in the table above. The increase is approximately 15%, except for those that are "held harmless". Part B (Outpatient/Medical) Deductible increases $19In 2015, the Part B deductible is $147. In 2016, it will increase to $166. See how this impacts Plan G and Plan F coverages. Part A Deductible & CopaysThe Part A deductible for the first 60 days of a hospitalization increases from $1,260 (in 2015) to $1,288 (in 2016).

If you get transferred to a skilled nursing facility as part of a hospitalization, the first 20 days are covered by Medicare. For days 21-100, there is a copay of $157.50/day in 2015. This is increasing to $161/day in 2016.  In our FREE guide for the Top 5 Biggest Mistakes people make on Medicare, the #2 biggest mistake is not properly analyzing and selecting your prescription drug coverage. Our mission at Senior Advisors is to help educate individuals on Medicare to ensure everyone has a clear understanding before making a decision about their coverage.To help you avoid making a mistake with Part D coverage, we have created a couple of short videos to help guide you and provide some additional information on Part D of Medicare. 2015 and 2016 Part D (Prescription Drug Coverage) OverviewUsing Medicare.gov tools for Part D Analysis and SelectionWe hope you enjoy these videos and most importantly, that you learn something about Part D of Medicare and avoid making a mistake that could be very costly.

If you would prefer to have someone assist you in reviewing your Prescription Drug Plan for 2016, you can fill out our online form for a FREE RX Analysis. Plan G could save you hundreds! This is a good opportunity to review your Medicare Supplement and Prescription Drug coverage to ensure you have the best value. You should learn about a Plan G which provides a great value and could save you hundreds of $ per year or more! Also, Plan F is no longer accepting new entrants starting January 1, 2020, which will impact premiums on Plan F and is another reason to look into a Plan G. Call now to see if you are eligible for a Plan G! 1-856-866-8900 or 1-908-272-1970 Best Regards, Justin Lubenow Senior Advisors justin@senior-advisors.com |

Justin LubenowSee bio here Categories |

RSS Feed

RSS Feed

|

Our Services

|

Company

|

|

Moorestown Office | 214 W. Main Street, Suite 101, Moorestown, NJ 08057 | Tel:856-866-8900

Servicing Moorestown, Cherry Hill, Mount Laurel, Haddonfield, Voorhees, Medford, Marlton, Philadelphia, surrounding towns, and licensed in 30+ other states as well. Cranford Office | 15 Alden Street, Suite 8, Cranford, NJ 07016 | Tel: 908-272-1970 Servicing Cranford, Westfield, Summit, Scotch Plains, Mountainside, Berkeley Heights, New Providence, Basking Ridge, surrounding towns, and licensed in 30+ other states as well. Phoenix Office | 20715 N Pima Rd, Suite 108, Scottsdale, AZ 85255 | Tel: 602- 935-8444 Servicing Phoenix, Scottsdale, Peoria, Sun City, Sun City West, Paradise Valley, Fountain Hills, Cave Creek, surrounding towns and licensed in 30+ other states as well. Email: info@senior-advisors.com (Se Habla Español -Tel: 908.481.5678) |

We do not offer every plan available in your area. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options. Not connected with or endorsed by the United States government or the federal Medicare program.

Copyright © 2023 Senior Advisors, LLC | Licensing & Legal | Privacy Policy

Copyright © 2023 Senior Advisors, LLC | Licensing & Legal | Privacy Policy