As part of the Medicare Advisory Group of National Association of Health Underwriters, we actively lobby for key issues that affect Medicare Beneficiaries. One issue that many individuals have been impacted by is Cobra as Credible Coverage. You can read more about these Cobra situations here.

HR 6184, The Medicare Enrollment Protection Act was introduced by Representatives Bob Dold (R-IL-10) and Kurt Schrader (D-OR-5) this week. The pending bill will allow individuals age 65+ with Cobra coverage to sign-up for Medicare Part B at any point during their Cobra coverage period. This bill is still pending, so until it passes the House & Senate, the current rules still apply which requires individuals age 65+ on Cobra to sign-up for Part B of Medicare within 8 months of losing their active employment status. We will continue to raise awareness of this issue and press to get this fix included in a later legislative package.

0 Comments

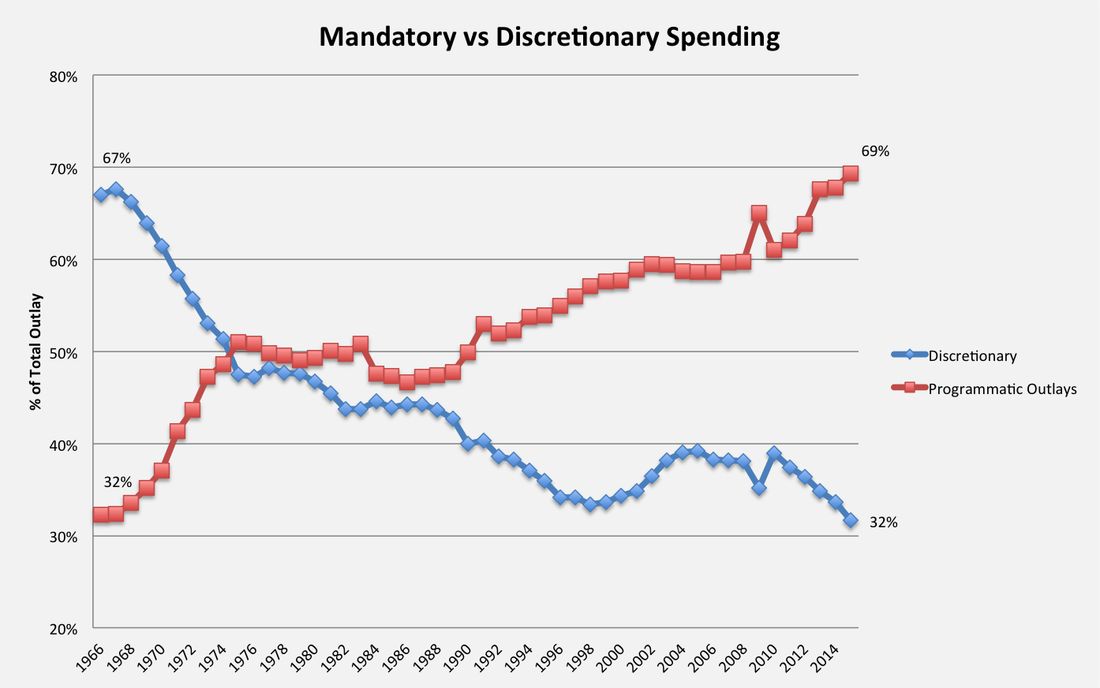

On Monday evening nearly 100 million people watched the first presidential debate. As expected, there was little substance from either candidate. I am not going to pick apart the entire debate but I am going to highlight the biggest economic issue this country is facing, which NEITHER candidate mentioned during the 90-minute debate. (It’s possible that I zoned out during one of the many diatribes and missed it.) What if… …you were making $120,000 per year (decent income, top 20% of income in U.S.), and 32% of your monthly income was immediately deducted each month. So, rather than $10,000 per month in take home pay, you would take-home $6,800 per month. This may not seem that far-fetched because we do have deductions/taxes that are in this realm of proportion. People find a way to pay their mortgage, utilities, food, insurance, and some discretionary spending with these deductions. What if that 32% commitment increased to 70%... ...leaving just $3,000 per month to pay for the same expenses? Would you be able to survive and pay for your home, food, utilities, and other discretionary spending? Would you be stressed?  Source: March 2016 CBO Historical Budget Data Mandatory Spending is now 70% of budget and increasing! In 1962, 32% of our U.S. budget went to Mandatory Spending (e.g. Social Security & Medicare) programs, and 67% went to Discretionary Programs (e.g. Military, and Other). In 2015, those percentages flipped to nearly 70% of the U.S. spending is going to mandatory programs, and this % will continue to increase over the next 10-15 years as more and more baby boomers are aging into Social Security & Medicare.  Source: March 2016 CBO Historical Budget Data

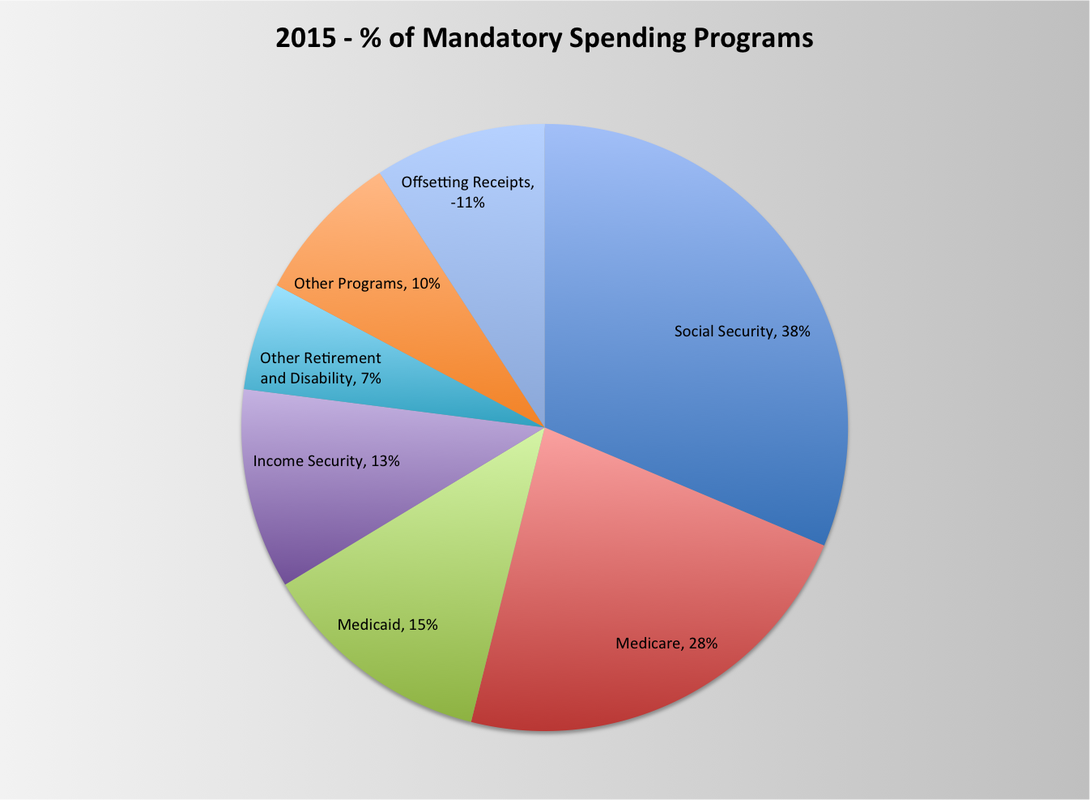

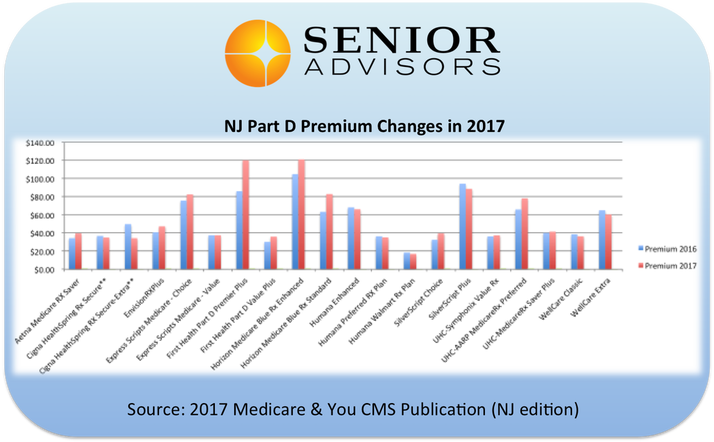

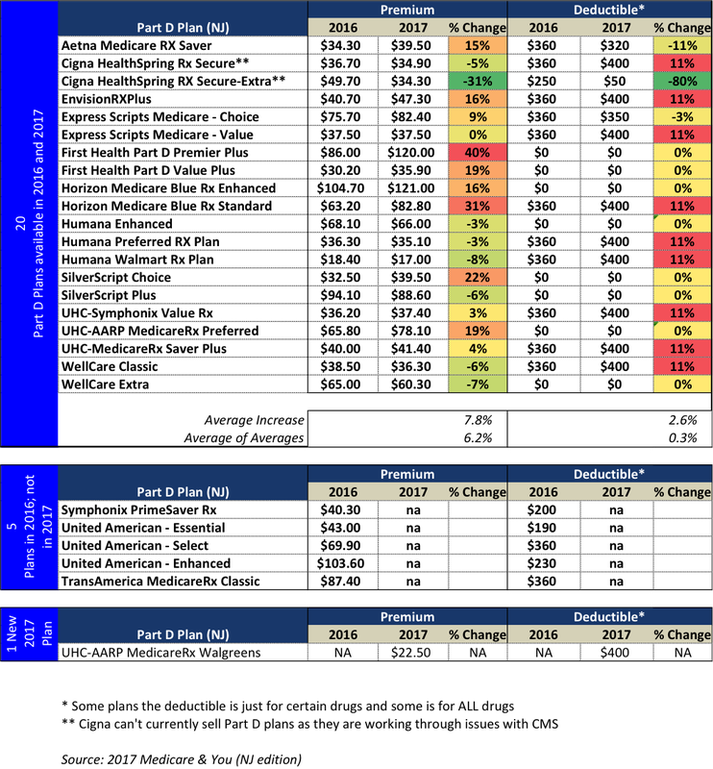

As we peel back the layers within the Mandatory Spending Programs, Medicare + Social Security make up about 2/3 of the Mandatory Spending. If we add in Medicaid, this increases to over 80% of our Mandatory Spending. As more and more dollars go towards Mandatory Spending Programs, we will not have funding for any “Discretionary” expenses such as Infrastructure, Energy, Military, etc. This will create National Security risks and infrastructure challenges that could set us behind other countries. Candidates focus on Economic Growth I understand both candidates are more focused on economic growth. I realize if we can grow the economy by 10-12% per year, these expense issues become less of an issue, because we will have revenues that can offset the increased expenses. But, this is similar to an individual (whose take-home pay dropped 50%) trying to out-earn their debt obligations and continuing to spend the same way. “I will just keep spending more and more on credit cards, but I know that I can make more money to cover the expenses and growing interest in the future.” This is wishful thinking and a recipe for financial disaster. Offending a large population of voters I suspect the campaigns are intentionally avoiding these two key programs (Medicare & Social Security) so they do not create any negative voting impact with a large population of voters. We should all be very concerned that these Programs are just not sustainable, and the longer we wait to address this Major Budget issue, the worse this problem gets and the more painful it will be to address. A few months ago – I wrote an article with some high-level thoughts on addressing the expense issues with these programs without impacting current beneficiaries on Social Security & Medicare. If you are interested, you can read that article here.  If you are currently a Medicare Beneficiary, you should have received your 2017 Medicare & You book from CMS (Center for Medicare & Medicaid Services) this week, or in the coming weeks. In this publication, you will find the 2017 Part D premiums & deductibles for each available plan in your area. We did some analysis on the NJ Part D premium & Deductible changes for 2017.  As you can see in the table, some plans actually reduced premiums (e.g. Humana Walmart went from $18.40/month to $17.00/month) and others had large increases up to 40% (First Health Part D Premier Plus went from $86/month to $120/month). For deductibles, some plans increased to the maximum deductible of $400, while others kept their $0 deductible. 5 Plans Not Available in 2017? There are five plans that are not currently showing up in the 2017 Medicare & You book for NJ:

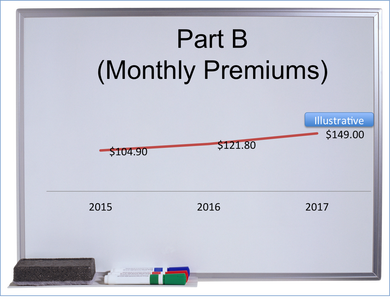

1 New Part D Plan in 2017 AARP has launched a new plan in 2017: UHC-AARP MedicareRx Walgreens for $22.50/month with a $360 deductible. This card will have preferred pricing at Walgreens, but does not require you to go to Walgreens. What if I don't live in NJ? We did not complete an analysis for all 50 states, but we believe the changes in other states will be directionally similar to NJ. You can find specific details about your state in your Medicare & You book that CMS should have mailed to you. Also, we will be able to look at 2017 pricing in other states on Medicare.gov starting in October. What's the best plan for you? The premiums and deductibles are just two of the inputs in the total cost equation. The 2017 Part D plans will be available in the next couple of weeks on the Medicare.gov Part D analysis tool which will allow us to determine which is the best Part D plan for each individual based on total overall cost for the year, which includes copays/coinsurance for your drugs in each of the key phases: deductible, Initial coverage, Coverage Gap, and Catastrophic Coverage. If you would like a FREE part D analysis, you can enter your Prescription info here and we will let you know the plan we would recommend for 2017.  Last year at this time, there were projections of a 50% increase in Part B premiums from $104.90/month up to $159/month. There was a lot of push-back and lobbying against this high of an increase - the end result was a 16% increase to $121.80/month in 2016. This increase only impacted certain groups of people due to the "hold harmless provision". Read more about which groups were impacted here.

For 2017, some are projecting an increase up to $149/month for individuals that are not held harmless - those not currently taking their Social Security benefits and in the first income tier (currently <$85k/year MAGI for single, <$170/year MAGI for filing joint returns). If an individual is currently taking Social Security benefits (and in the first income tier), the Part B premiums cannot increase at a greater rate than the Social Security COLA due to the 'hold harmless provision". So what does this all mean? At this point - not much. It is just a guideline for what "could happen". The government didn't actually finalize the 2016 changes until Oct 30, 2015 so it's very possible we may not know the final decision on Part B premiums (or deductibles) until the end of October again. If you Part B premiums do increase, it is a great time to shop for the best Medicare Supplement available to make sure you offset any increases in premiums with some savings with your Medicare Supplement. People switching from a Plan F to a Plan G save an average of $500-600/year in premiums and the only difference in coverage is the Part B deductible ($166 in 2016). If you would like a FREE quote for a Plan G to see if you have the best value, Call now (1-908-272-1970) Cranford Office or (1-856-866-8900) Moorestown Office

|

Justin LubenowSee bio here Categories |

RSS Feed

RSS Feed

|

Our Services

|

Company

|

|

Moorestown Office | 214 W. Main Street, Suite 101, Moorestown, NJ 08057 | Tel:856-866-8900

Servicing Moorestown, Cherry Hill, Mount Laurel, Haddonfield, Voorhees, Medford, Marlton, Philadelphia, surrounding towns, and licensed in 30+ other states as well. Cranford Office | 15 Alden Street, Suite 8, Cranford, NJ 07016 | Tel: 908-272-1970 Servicing Cranford, Westfield, Summit, Scotch Plains, Mountainside, Berkeley Heights, New Providence, Basking Ridge, surrounding towns, and licensed in 30+ other states as well. Phoenix Office | 20715 N Pima Rd, Suite 108, Scottsdale, AZ 85255 | Tel: 602- 935-8444 Servicing Phoenix, Scottsdale, Peoria, Sun City, Sun City West, Paradise Valley, Fountain Hills, Cave Creek, surrounding towns and licensed in 30+ other states as well. Email: info@senior-advisors.com (Se Habla Español -Tel: 908.481.5678) |

We do not offer every plan available in your area. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options. Not connected with or endorsed by the United States government or the federal Medicare program.

Copyright © 2023 Senior Advisors, LLC | Licensing & Legal | Privacy Policy

Copyright © 2023 Senior Advisors, LLC | Licensing & Legal | Privacy Policy